America has a well-earned reputation as the land of opportunity, where people have the ability to enhance their lives personally and professionally. At the same time, around half of Americans report living from paycheck to paycheck, and almost a third of households spend 90% of their income or more on meeting their basic needs. Overcoming this situation depends on knowing what to do and building the right habits, but financial stress can cloud the vision.

If you're tired of living paycheck to paycheck or concerned you may be headed in that direction, you still have hope. Countless Americans have gone from money struggles to financial peace by applying the tried-and-true principles explained in this guide, and so can you.

What Does Living Paycheck to Paycheck Mean?

Living paycheck to paycheck is when you have no or barely any money left to save or pursue financial goals after covering regular expenses.

If you live paycheck to paycheck, affording your bills may not be feasible if your next paycheck is late. You may spend almost an entire month's salary on that month's expenses. You may even feel like you can't afford to live on your wages right now.

The good news? You can improve your situation, but first, you need to understand it.

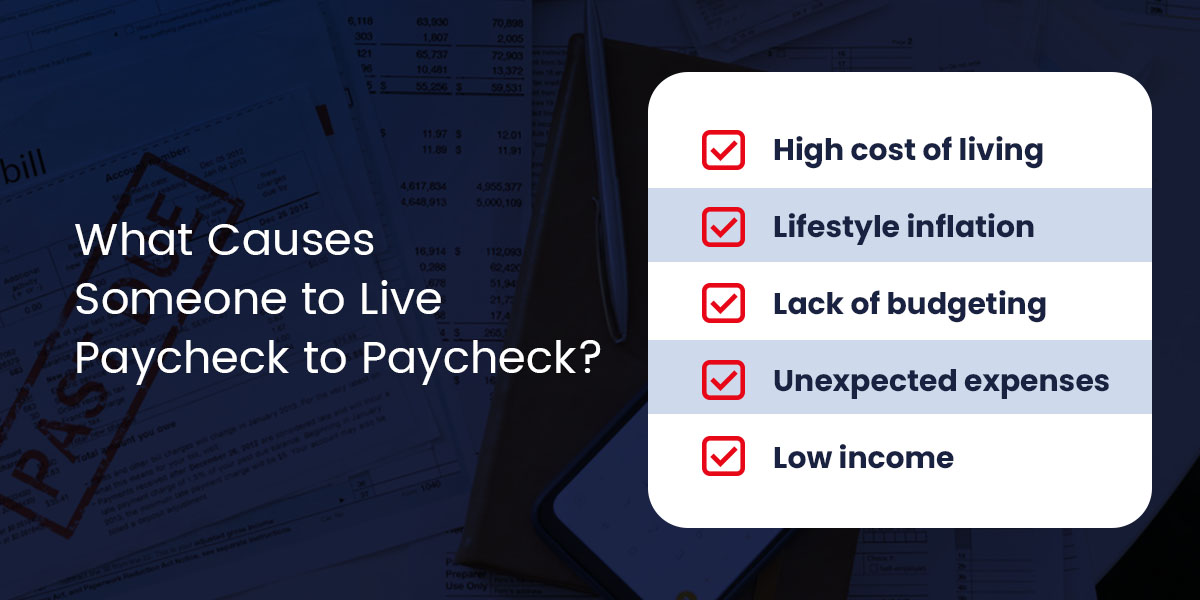

What Causes Someone to Live Paycheck to Paycheck?

Most people who live paycheck to paycheck find their expenses exceed their income for one or more of these five reasons:

- High cost of living: From 2014 to 2024, the United States Consumer Price Index (CPI) rose from 236.736 to 313.689. This means something that cost $100 in 2014 would cost $132.51 in 2024. As the cost of living rises faster than household income, more families end up living paycheck to paycheck.

- Lifestyle inflation: Most people spend more to improve their standard of living when their income rises, so their expenses continue eating up their paychecks even as those paychecks grow.

- Lack of budgeting skills: Many Americans are unsure how to create and stick to a budget that supports their financial goals.

- Unexpected expenses: Unforeseen costs like emergency medical bills or car repairs can lead to debt for unprepared households.

- Low income: Earning a lower salary can make it challenging to cover your necessities and have money left over.

You have more control over some of these factors than others, but there are steps you can take to overcome or at least offset every one of them.

How Not to Be Broke in 8 Simple Steps

Whatever your starting point, you can take action today and discover how to not live paycheck to paycheck. Here are the eight steps anyone can follow to move from barely making ends meet toward financial peace.

1. Assess Your Financial Situation

To plan your route to financial peace, you need to know where you are now. Start by tracking your income and expenses using an app, spreadsheet or pen and paper. Use whichever method feels easiest for you to start right now — this is the first step to discovering how to save money every paycheck. Record the following:

- What do you earn in a typical month?

- What do you spend your money on?

- Which of your expenses are needs, like rent, groceries, or health care?

- Which expenses are wants, like streaming services or restaurant meals?

It's also helpful to know your financial goals, as these will motivate you and guide your decisions. Whether you want to save for a kid's college fund or afford an annual vacation, reflect on what financial peace would look like for you 10, 20, or 30 years from now.

2. Create a Budget

Starting with what you learned from your financial self-assessment, it's time to make a realistic monthly budget. To help shape your budget, convert one or more of your big-picture financial goals into a specific, measurable, achievable, realistic, and time-bound (SMART) objective you can pursue right away. For example, you could set a target of saving $10 a week toward an emergency fund by unsubscribing from unnecessary streaming services and make sure your budget aligns with this.

Many people benefit from using the 50/30/20 rule for budgeting. This means using 50% of your income for needs, 30% for wants, and 20% for savings. Consider this a starting point and adjust it based on your circumstances and goals. Ensure your budget for each month includes:

- Total monthly income.

- Fixed expenses that are the same every month.

- Variable expenses that change monthly.

- Savings and debt repayments.

Mark all your expenses as either needs or wants so you can prioritize needs and reduce spending on wants to free up more money if necessary. A good budget gives every dollar a job, meaning anything left over can go toward specific goals like saving for retirement.

3. Reduce Expenses

Though it may feel difficult, cutting unnecessary costs is the simplest way to save more money every month. Focus on expenses marked as wants and consider what you can remove. Most people could afford to reduce spending on vacations, luxury clothing, eating at restaurants, drinking at bars, or unnecessary memberships and subscriptions. You can even look for ways to reduce spending on some of your needs by shopping at more affordable stores or using coupons and rewards programs.

All kinds of emotional and psychological triggers can influence our spending habits. Be kind to yourself, but practice mindfulness and build the skill of delaying gratification as you reflect on impulses to buy and whether acting on them supports your financial goals. Understanding the motivations behind your money choices can help you improve them over time.

4. Address Your Debt

Debt is one of the top causes of financial anxiety for Americans, and it may contribute to mental and physical health issues. Reducing what you owe is the path to fewer monthly payments and more money to save toward your goals. Here are four strategies to help you get out of debt when you're living paycheck to paycheck:

- Get rid of credit cards: If you want to be debt-free, you first need to avoid adding more deficits, especially credit card debt. The average American credit card has an interest rate of over 20%, making this one of the most expensive forms of debt. Some people cut up their credit cards for a fresh start, but if you want to keep yours, use it for amounts you know you can repay and make those payments before interest kicks in.

- Prioritize debt consolidation: One way to save on interest is to consolidate several outstanding balances into one by taking out a new loan to repay the others. For example, if you have two credit card debts of $400 at 20% annual interest each and a $200 medical debt at 10% interest, a personal loan of $1,000 at 8% interest could cover all your debts. Comparing the two scenarios, you would save $100 in interest after the first year by consolidating.

- Use the avalanche approach: This approach means paying off all your debts one at a time while making minimum payments on the others, starting with those that have the highest interest rates. The avalanche method could save you the most money on interest over time, though progress can feel slow at first.

- Try the snowball method: This method means paying off all your debts one at a time, from the one with the smallest balance to the largest, while making minimum payments on the rest. Compared to the avalanche approach, your total spending on interest will be higher, but many prefer the snowball method because of the quick, motivating wins. Everyone with multiple debts can benefit from one of these methods, and the right one for you depends on what motivates you more.

5. Increase Your Income

The more you can raise your income, the more money you can save with the help of the other strategies in this guide. The two basic ways to increase your income are earning more within your current occupation and adding a secondary activity.

Although it can feel intimidating, the lowest-hanging fruit is to negotiate a raise based on your performance and the market rate for your job. If your employer declines, ask what you could do to create more value and justify earning more. They may point you to professional development opportunities or ways to contribute more to your company's strategic goals. If you don't see a raise on the horizon, you could consider putting in extra hours or applying for similar roles at other companies that pay more or have better career advancement opportunities.

If you can make the time, your other option is to start a side hustle or a second job. You can get creative with your skills, but some popular supplementary income streams include:

- Babysitting.

- Paid surveys.

- Selling cooked or baked goods.

- Driving for a ride-hailing or delivery service.

- Tutoring.

- Other freelance services, from graphic design to software development.

As a bonus tip, make a habit of selling anything you don't need, from clothes and books to electronics, for extra cash.

6. Build an Emergency Fund

An emergency fund is a lump sum you set aside for unexpected expenses, like urgent car repairs or medical bills your insurance won't cover. This sum gives you some peace of mind, covers important costs that pop up beyond your budget and reduces your risk of going into debt to handle these expenses.

A good rule of thumb is to save enough for three to six months of necessary expenses, but even a small amount can help protect your progress toward your financial goals.

Once you've worked out how much you can save by reducing expenses and increasing income, try using the set-and-forget approach for saving when living paycheck to paycheck. By setting up an automatic transfer of $100 to a separate savings account each month, your emergency fund can reach $2,400 in two years. You can also reach your goals faster by contributing any extra money from gifts, bonuses, or selling household items to your savings.

7. Educate Yourself

Arming yourself with financial knowledge is crucial to defeating the paycheck-to-paycheck cycle. The more you can learn, the better informed your decisions will be, and taking in positive, actionable financial advice can help you stay motivated. Good sources of financial information include:

- Personal finance blogs with guides.

- Qualified financial advisors.

- Budgeting workshops.

- Online courses.

- Books.

- Podcasts.

Having a financial accountability partner to share resources with can also help you stay on track as you apply what you learn. This could be your spouse, a friend, or a fellow workshop attendee.

8. Be Patient

To stop living paycheck to paycheck, you need to put your knowledge into practice with good habits that take time to form — and often more time to yield life-changing results. Some financial goals take years to achieve, so be patient and give yourself grace as you adjust to lifestyle changes on your road to financial peace. Along the way, celebrate wins like saving your first $10 for your emergency fund or reducing your list of debts by one. The journey may take time, but a wealthier future is waiting to congratulate you.

Why Trust Atlas Credit?

Since our founding in 1968, Atlas Credit has grown into one of the most responsible and reputable personal lenders, with over fifty locations in Texas and Oklahoma, as well as a responsible online lending service. In our decades of experience providing personalized customer service to people in diverse financial situations, we have seen the various circumstances that can lead to living paycheck to paycheck. We have also helped implement the strategies that enable countless people to move toward a brighter financial future.

Every employee at Atlas Credit is on our team because of their expertise and professionalism in the financial industry, meriting the highest commendations from our customers. We are committed to responsible lending, so our team is experienced in helping customers understand their financial situation better before we lend. This includes analyzing their income, expenses, debts, and budget to provide trained affordability guidance.

Experience Financial Relief With Atlas Credit

By following the steps in this guide and building smart financial habits, you can stop living paycheck to paycheck and experience financial peace. Along the way, you may have debts you want to consolidate or unforeseen expenses your emergency fund isn't ready to absorb. If that happens, you can contact Atlas Credit for easy, affordable personal loans.

At Atlas Credit, we consider more than your credit score for approval and will look at your budget with you to help find a loan and repayment plan you can afford. Plus, we make it quick and simple. You can apply for a loan in minutes using our online form.

Apply for a personal loan today to experience financial relief.