Are you wondering how to budget money? Knowing how you manage your income and expenses can relieve financial pressure, get you out of debt and help you achieve your dreams. Setting goals to save toward can motivate you to spend wisely. There are several effective budgeting strategies, but the best one is the one that works for you. Budgeting is a personal process, and you should feel confident you can manage whichever method you choose. Let's look at some of the best ways to budget money.

Set Financial Goals

When you create your budget, it's important to have financial goals. You should have short-, medium- and long-term goals to work toward. Attaching motivation and why to your goals will help you to stick with them. Here's what your goals may look like:

Short-Term Goals

Short-term financial goals are a good starting point and will give you the confidence boost to save for bigger goals. Consider the following short-term goals:

- Emergency funds: When unexpected events arise, you'll be happy to have an emergency fund. Unemployment or medical emergencies are some of the reasons why having an emergency fund is critical. A good goal is to save three to six months of income in your emergency account.

- Pay off credit cards: If you have multiple credit card debts, list them from the highest interest to the lowest. Pay the minimum amount on all except the card with the highest interest — your aim should be to pay off the most expensive debt as quickly as possible.

Medium-Term Goals

Once you reach your short-term goals, you can move on to your midterm goals. Let's look at some medium-term financial goals:

- Life insurance and disability insurance: If you have a spouse or children who depend on you financially, you must have life insurance and disability insurance. These policies ensure your loved ones have a source of income if you pass away or cannot work.

- Pay off student loans: Student loans can strain your finances. By paying off your loans, you can free up more money to save for your other goals.

- Save for your dreams: You may want to save for your dream home, buy a new car or take a vacation.

Long-Term Goals

The most common long-term goal for people is saving for retirement. A general rule of thumb is to save at least 10% to 15% of your income in a tax-advantaged retirement account such as a 401(k) or 403(b) if you have access to one. A traditional IRA or a Roth IRA are other forms of retirement savings accounts.

Calculate Your Income and Expenses

To create a suitable budget for each month, you'll need to list your income and expenses. You can use an app, paper or a spreadsheet to draw up your budget.

1. List Your Income

Your income is the money you expect to receive during the month. This income may be in the form of paychecks, investment income, money from a side hustle, freelance work or any other form of payment you expect to come your way. Record each source of income on a separate line. If your income is irregular, use the lowest income month from the last six months in your budget. You can adjust the budget if you receive more money and put it toward one of your financial goals.

2. List Your Expenses

Expenses are how you spend your income. Pay yourself first, so add a line for your emergency fund, savings or dream. Next, cover all your essential expenses — utilities, food, transport and shelter. Move on to other significant expenses like insurance, child care and debt. Then, list non-essential expenses, such as entertainment and eating out. Listing your costs helps you see where you spend the most money. You can cut down on non-essentials to help you meet your financial goals.

Be mindful that unexpected expenses may come up, so do your best to think of all the scenarios that your budget should consider.

3. Subtract Your Expenses From Income

This last step will show you how much money you have left after your expenses. If you have extra income left over, you can allocate it to a goal instead of spending it aimlessly. If you have a negative balance, you'll need to look for places to increase your income or reduce your expenses. Non-essential items are a good place to start.

Evaluate Needs vs. Wants

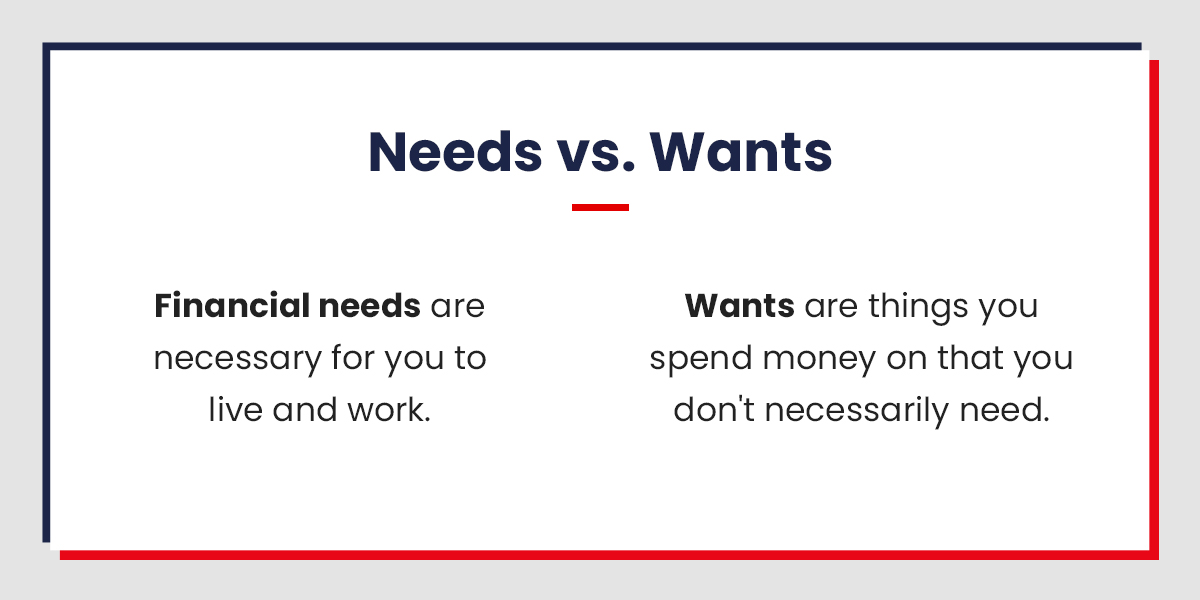

When categorizing your expenses, it's important to understand the difference between wants and needs.

Financial needs are necessary for you to live and work. These costs usually make up most of your expenses. You may have the following listed as needs:

- Food

- Phone

- Utilities

- Insurance

- Transportation

- Mortgage or rent

Wants are things you spend money on that you don't necessarily need. They are fun luxuries that you can live without but enjoy having. For example, you need food, but eating out every night is a want. Some of your wants may include:

- Travel

- Eating Out

- Entertainment

- Designer Clothing

When considering your wants and needs, remember that yours may be unique. For example, some people see a car as a want, whereas a car may be necessary for your work.

Carefully analyze each category and ask yourself if it is a need. You may be able to reduce some of your necessary expenses, such as shopping for more affordable insurance or purchasing some of your groceries in bulk.

Test out Different Budgeting Methods

When creating your budget, you can try out a few personal budget models to help you take control of your spending and reach your goals. The best method is the one you can stick with.

50/30/20

The 50/30/20 rule recommends putting 50% of your income toward your needs, spending 30% on wants and saving 20% of your income. This means you'll use 50% to pay for bills that you have to meet every month, such as utilities, rent or mortgage, health care, and child care. Allow yourself to spend 30% of your income on wants — things you enjoy but don't need to live. Lastly, put 20% toward savings and goals like an emergency fund or paying off debt.

Pay Yourself First

With this method, you put money into your savings, emergency fund, retirement or any other goal first before you spend your money on anything else. When you start by paying yourself first, your spending automatically adjusts to what you have left in your budget. This method can be effective because it prevents you from spending money you should be saving. Ideally, you should save between 10% to 20% of your monthly income.

Zero-Based Budget

A zero-based budget allocates all your income toward expenses, savings goals and debt payments. When you deduct your expenses from your income, you should have a zero balance. This way of budgeting is very different from living paycheck to paycheck because all your expenses are met at the end of the month.

Zero-based budgeting can help you be more aware of the money flowing in and out of your account, which can prevent you from overspending. You'll need to monitor your expenses closely. Variable expenses can easily sneak in and throw your spending off track.

Envelope Budget

When you use the envelope method, you put your cash into separate envelopes, physically or online, for different needs. These envelopes serve different categories, such as groceries, entertainment, utilities and clothing. You assign each envelope an amount, and once you've spent the money in that envelope, you're done until you add more money the next month.

This method makes overspending difficult because you can only use what is in the envelope for that month. If you have leftover cash, you can put it toward savings or one of your goals.

Take out a Personal Loan From Atlas Credit

Budgeting is critical for staying on top of your expenses. Evaluate your income and expenses to find areas where you can cut back and save more money. There are various budgeting techniques, such as paying yourself first and the envelope method, that can help you stay on track. Having goals to work toward will also motivate you to monitor your expenses and keep your spending in line.

You may have done everything you can and still need more money to supplement your income. A personal loan can help you manage your expenses and get back on track. At Atlas Credit, we provide a simple and easy online loan application process — it only takes a few minutes. To learn more, apply online for a loan today!