Loans are borrowed money that needs to be paid back, typically with interest. Loans can be used to cover big payments, like the cost of a house or college, since most people can't readily spend that much money. Borrowing money is a big financial decision that can affect your financial position for the rest of your life. Make sure you understand how taking out a loan works and what to know about taking out a loan before applying for one.

From interest rates to the application process, having some tips for taking out a loan can help ensure you're making smart financial decisions.

Things to Consider Before Taking a Loan

Taking out a loan is a serious decision to make with great consideration. Loans are typically significant amounts of money that you wouldn't have upfront. While being able to borrow money is extremely helpful for many people, you need to be careful about the loan you get and how you go about getting it. To help you make the most informed decision, here are a few questions to ask yourself before taking out a loan and general things to consider.

Why Do You Want a Loan?

Loans help people finance nearly anything. Sometimes, loans are used unnecessarily, so it's important to consider what you want the loan for and whether you need the money immediately or could wait and save up your own money. Here are a few common reasons you may want to take out a loan:

- Home mortgage: Put simply, buying a house is expensive. Most people don't have the funds to buy a house with cash or even a check. In this case, you'd finance a new home with a loan so you can pay it off over time.

- Vehicle financing: Similar to a house, most people can't afford to purchase a new car out of pocket. Even used cars can be out of reach without a loan. Loans allow you to finance a vehicle on the spot.

- Home improvements: You may need a loan to make home improvements or remodel. Building an addition, remodeling a bathroom, or replacing all your appliances can add up quickly. With a loan, you can make these dreams a reality without having the money in your pocket.

- Education: One of the most common reasons for taking out a loan is for education. College and other forms of higher education can cost tens of thousands of dollars per semester. The cost seriously adds up over four or more years. Loans make education more accessible for more people.

- Wedding expenses: In 2021, the total cost of a wedding was an average of $34,000. It's common for couples to use loans to cover the cost of wedding components, like the venue, dress, flowers, and more, to avoid draining their savings accounts.

- Emergency expenses: Emergency expenses can take you by surprise. If you suddenly need to cover medical bills, funeral costs, or other emergency expenses, you may consider taking out a loan to finance these unexpected costs.

- Moving costs: Moving your belongings from one location to another can be costly, especially if it's a long-distance move. Whether transporting your belongings, purchasing new furniture, or transporting your car across the country, a loan can help you cover the costs without tapping into your savings.

- Debt consolidation: If you have multiple credit cards or loans you owe money on, you may get a new loan to pay off all the others so you only have one to make monthly payments on. This can be beneficial, especially when your new loan has a lower interest rate.

How Much Money Can You Afford to Take Out (and Pay Back)?

A loan is borrowed money, which means it needs to be paid back. Many lenders will give you a grace period after receiving the loan, then monthly payments on the loan start. In many cases, you'll have options regarding the monthly payment amount, interest rate, and length of time you'll repay the loan. This is one of the biggest financial decisions to make because it determines the total amount you'll pay back. The longer you take to repay the loan, the more interest it accrues, and the more you end up paying.

For example, let's say you want to take out a $10,000 loan. The lender may give you two repayment options:

- Monthly payments of $188.71 over five years with a 5.00% annual percentage rate (APR)

- Monthly payments of $304.22 over three years with a 6.00% APR

While the first option may look like the more affordable choice because it has a lower monthly payment and APR, it's actually the more expensive option. If both are paid off on time, the first option would cost $11,322.74, and the second would cost $10,951.88. Despite having a higher interest rate, the second option gets the loan paid off much sooner than the first option, so less interest accumulates over the shorter time frame.

Be sure to consider repayment options carefully. Just because you can afford a lower monthly payment doesn't mean you can afford the loan over time.

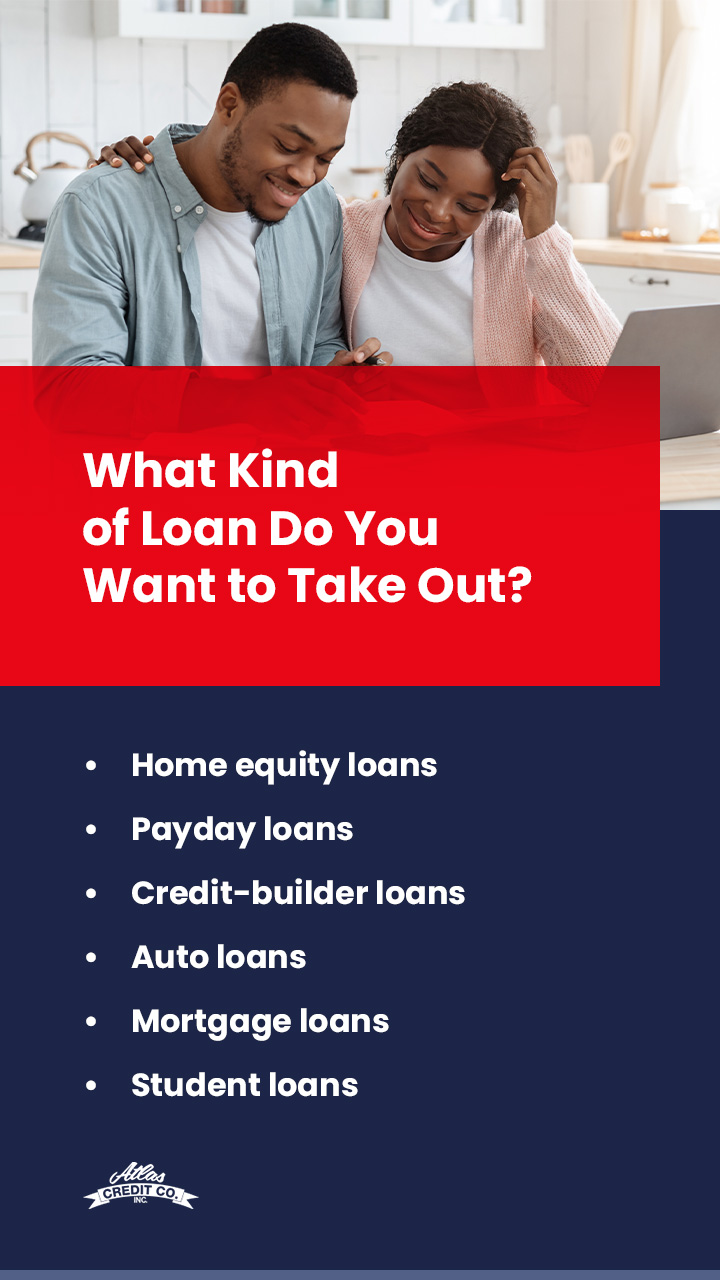

What Kind of Loan Do You Want to Take Out?

Your needs will likely determine what type of loan you'll take out, though some can be used for various needs. For example, personal loans can typically be used for whatever you want. If you're using a loan to pay for a wedding, emergency expenses, or home improvements, you'll likely get a personal loan. Depending on the lender and the amount borrowed, personal loans may be repaid over a few months or several years. They can also have fixed or variable rates.

Here are several more common types of loans you could take out:

- Home equity loans: Home equity loans let you borrow a percentage of your home's equity to use for whatever you want. You'll receive a lump sum and repay it in monthly installments over five to 30 years. Similar to a home equity loan, a home equity line of credit (HELOC) works like a credit card in which you can draw from a credit line during specified draw periods, then pay off the loan within 20 years. Home equity loans typically have fixed rates, while HELOCs have variable rates.

- Payday loans: Payday loans are the riskiest and often most expensive type of loan you generally want to avoid. These types of loans let you borrow anywhere from $50-$1,000 without a credit check, making them the easiest to get. However, they need to be fully repaid by your next payday. Many borrowers struggle to do so and end up renewing the loan, which results in heavy fees, high-interest rates, and an endless cycle of debt.

- Credit-builder loans: If you have no or poor credit, you can use a credit builder loan to improve your credit score. These generally don't require a credit check and are often for smaller amounts of money, which gets put in a savings account as you make monthly payments over six to 24 months. Once the loan is repaid, you get your money back. These loans show major credit bureaus that you've improved your credit and can make timely payments.

- Auto loans: Auto loans are generally easy to get. You'll borrow the price of the car and typically pay it back between 36-72 months, depending on the terms. Most auto loans use the vehicle you're buying as collateral, which means the lender can repossess the car if you stop making payments.

- Mortgage loans: Mortgage loans let you borrow the price of a house minus your down payment. Like auto loans, your property is collateral and can be foreclosed if you stop making mortgage payments. Mortgages can be repaid over 10-30 years and have fixed or adjustable interest rates.

- Student loans: There are two types of student loans — federal and private lenders. The U.S. Department of Education funds federal student loans, which means students with the same type of loan have the same terms, interest rates, fees, and repayment periods. Federal student loans are more desirable because they usually don't require credit checks and offer benefits like forbearance, deferment, income-based repayment, and forgiveness.

Secured vs. Unsecured Loans

Most types of loans are either secured or unsecured, which ultimately refers to whether or not they're attached to collateral. Secured loans are attached to something so lenders can easily claim their money if you stop paying. The most common secured loans are mortgage and auto loans. Secured loans are easy to get because lenders can easily repossess your property to get the money you stopped paying.

Unsecured loans are the opposite. They aren't attached to collateral, so if you stop making payments, the lender has to take legal action against you to collect payment. Taking legal action to receive payment can be a long process. Since unsecured loan lenders cannot quickly collect from you if you stop repayment, these loans are riskier to hand out, making them harder to get. Unsecured loans typically require pristine credit scores and history.

Your Credit Score

Your credit score is a significant factor when taking out a loan. Your credit score and credit history show how much debt you have and how well you make timely payments on that debt. Your score is based on numerous factors, including your payment history, how long you've had debt, new credit, types of credit, and more. Payment history is most important, as lenders want to see that you're likely to repay the loan.

A good credit score can affect your interest rates and monthly payments. The better your credit score is, the lower your rates and payments will likely be. People with low credit scores are less likely to be approved for a loan unless they have a co-signer with good credit. A co-signer becomes responsible for repaying the loan if you fail to do so.

Knowing your credit score is important so you know where you stand and what types of loan terms you may be eligible for. The best way to determine your credit score is by using a free score calculator online. Many banks and lenders also offer credit score calculators.

Your loan can either positively or negatively affect your credit score. Making payments on time and successfully paying off the loan can help build your credit. On the other hand, failing to make payments, paying late, or ignoring the terms of the loan can negatively impact your credit score, which will cause issues next time you try to get a loan.

Details of the Loan

Before signing for your loan, you must ensure you completely understand your loan details. Fully read the loan terms to understand the APR and any hidden fees you may encounter down the road. As mentioned above, the APR can significantly affect how much money you repay on the loan over time. Depending on your rate, you could pay significant interest amounts. Be sure to compare APRs for different loan options, like in the above example, to be sure your financial decision is logical.

Be sure to check the terms for hidden fees or ask the lender about them since they aren't always brought to your attention. Here are some common fees to watch for:

- Prepayment penalty: Some lenders charge a fee if you pay the loan earlier than expected. This is a method used to ensure the lender gets the full interest amount.

- Late fee: Late fees are charged when your monthly payment is late. This will also harm your credit score.

- Failed payment fee: If your account balance is too low to cover a payment you tried to make, the payment will fail. You may be charged a fee when this occurs.

- Loan processing fee: Most common with mortgage loans, a loan processing fee is often charged during the application process.

Know Your Loan Options

There is an abundance of ways to obtain a loan, which can be helpful when weighing your options. If there's a bank you already have a relationship with — for example, you may have a checking and savings account with them — it can be quick and easy to sit down and get approved for their loans. However, shopping around online can be a great way to find online lenders and other loan options, depending on how much you want to borrow.

For example, you can apply for a personal loan through Atlas Credit Co. online without using your credit history. Lenders like Atlas Credit help people with lower incomes get approved for loans with good terms and build their credit. These lenders can be more beneficial because they'll look at your situation and help you determine the best loan for your needs. They can even provide resources on what to know before taking out a personal loan.

Apply for a Personal Loan Online

If you're taking out a loan for the first time, you may feel overwhelmed with things to consider before taking a personal loan. At Atlas Credit, we make the online application process quick and easy. We help underserved applicants get the credit they need. We'll work with you and your financial budget to find an affordable solution for you. Apply online, and we'll get in touch with you, or contact us for more information on what to know about personal loans!