Refinancing your current loan is an excellent option for various circumstances, but it can also temporarily decrease your credit score.

In this article, you'll discover how refinancing impacts your credit, how the refinancing process works, and how to limit negative effects. You'll also learn some refinancing tips to help you make this significant financial decision.

What Is Refinancing?

Refinancing refers to the process of renegotiating the terms of a loan. This includes revising an existing loan and taking out a completely new loan to replace the old one. People typically choose to refinance their loans to improve the terms of the loan and make it easier to repay.

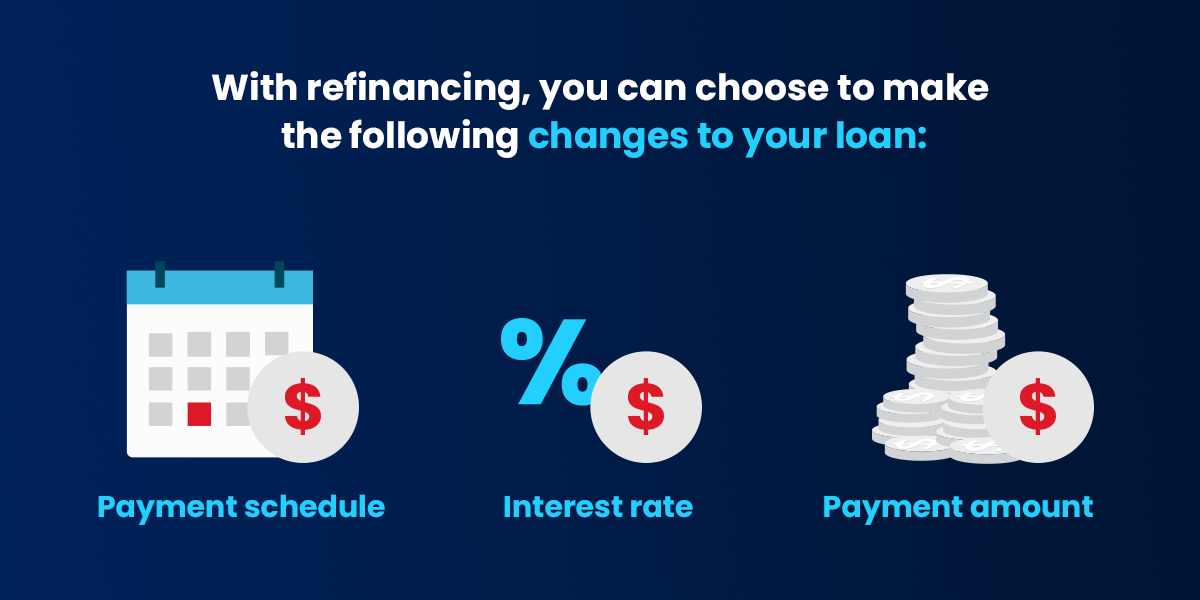

With refinancing, you can choose to make the following changes to your loan:

- Payment schedule: You can reduce or extend the repayment period of your load depending on your needs.

- Interest rate: If interest rates drop, you can negotiate a lower interest rate and save on monthly payments.

- Payment amount: You can increase or decrease your monthly payment amount, which will affect how long you have the loan.

Will Refinancing Hurt Your Credit?

Your credit score lets lenders know how likely it is you'll repay a loan, and the most widely used credit score is the FICO Score. This score weighs various factors to determine your score, such as payment history, utilization rate, credit age, new credit, and credit mix.

Refinancing a loan can lower your FICO Score and other credit scores temporarily. If you consistently comply with repayment amounts, your credit score will eventually pick back up. The initial dip is due to the following reasons:

- Hard credit checks: Applying for a new loan or increasing the credit limit on an existing loan counts as a "hard check" on your credit history, which can lower your score. This is because hard checks indicate you're acquiring more debt. These checks can linger on your credit report for around two years.

- Multiple loan applications: If you're shopping around for different loans over a long period of time, each inquiry will add a hard check to your history and greatly reduce your score.

- Extra debt: If your lender closes your existing loan instead of reworking it, it will be labeled as a "new" loan. Taking on new loans will decrease your credit score.

- Reduced loan age: Having older loans in good standing improves your credit score, as it presents a proven track record. Replacing an older loan with a new one will erase this history and decrease your credit score

Who Should Refinance?

Before refinancing, you should consider your unique financial and debt situation. Examining your credit history gives you insight into whether refinancing is a sound decision and if it is worth the potential savings. Refinancing is beneficial in specific circumstances, but at other times, refinancing can be unfavorable if you cannot afford the repayments or secure a lower interest rate.

Here are a few circumstances where refinancing is likely a good idea:

- You need to decrease payments: If your income decreases or expenses rise and you can't make your loan payments, you can refinance your loan to lower your monthly payments. While lower payments will generally increase repayment periods and subsequently increase the total interest paid, your credit score will be better off.

- You want to shorten the term: Refinancing your loan to a shorter term will clear the debt sooner and reduce the total interest amount. This is a good idea if your budget allows for increased monthly payments.

- Your credit score has improved: If you have paid off other debts and have a low debt-to-income ratio, then you likely have a better credit score. With a higher credit score, you can typically receive lower loan interest rates and save money.

- Interest rates have lowered: Sometimes — such as during economic decline — the general loan interest rate decreases. During this time, it's beneficial to refinance and lower the interest rate so you pay less monthly.

Does Refinancing Cost Money?

Sometimes, refinancing a car, home, personal, or student loan costs money. How much it costs depends on how you refinance the loan, the lender's fees, and what type of loan it is. You can determine if the costs are worth it by comparing them to your refinance cost savings. If you are adjusting an existing loan, you may not have to pay any fees. Always check the fees before you make a decision.

Some common refinancing costs include:

- Application or origination fee

- Termination fee

- Prepayment penalty fee

How to Refinance and Protect Your Credit Score

While refinancing can reduce your credit score, it's usually only temporary. You can use the following refinancing steps as a guide to help the process go smoothly and reduce the impact on your credit score.

1. Try to Achieve a Better Credit Score

Before you start, know what credit score you need for a loan so you have a target. If you already have a good credit score, you will likely secure more favorable interest rates. You can improve your score by taking action, such as reducing your current utilization rate and making timely repayments on other loans.

2. Prequalify for a New Loan

Prequalification involves requesting that a bank review your credit score before you apply for a loan. These checks count as "soft checks," which leave your credit score untouched. You can prequalify with multiple lenders to see potential rates and terms on a new loan.

Prequalification is important because you will receive a hard check when you apply for a loan, even if they end up rejecting you. You can reduce the number of hard checks by prequalifying, which lets you know if you'd be approved without formally applying for a loan. Sometimes, lenders don't offer prequalification. In this case, it's a good idea to submit your applications simultaneously or at most within 14 days of each other. This makes your multiple applications only count as one hard inquiry, which reduces their negative impact.

3. Compare the Loan Rates and Terms

Next, compare the new loan offers to your existing one. Ensure the new rates and terms offer you the payment period, monthly amount, and interest rate you want.

4. Consider Any Refinancing Costs

The last thing you want is a surprise bill from either your current lender or the new loan originator for fees such as paying it off early and initiating the new loan. It is best to know about these beforehand, even though they tend to be minimal.

5. Apply for the New Loan

After choosing your new preferred lender, you'll complete an official application and provide all the necessary documentation. Most banks and lenders require proof of identity and income, at the least. Once you submit your application, the lender will do a hard credit check, which will only impact your credit score slightly.

6. Use the New Loan to Repay the Original

After you receive the approval and the funds are in your bank account, use this money to honor your previous loan in full. For your convenience, some lenders may pay off your first loan directly.

7. Confirm the Original Loan Is Closed

Check your account to ensure the first loan's balance is gone, or if the loan is not with your bank, request confirmation that the account is closed to avoid any further fees or penalties.

8. Begin Payments on the New Loan

You can focus on the new loan and set up automatic, recurring payments from your account so you have one less thing to remember. Ensuring timely monthly repayments is essential to improve your credit score.

Get a Quick Personal Loan From Atlas Credit

Refinancing a loan is a big step in securing your financial and credit health. At Atlas Credit, we understand how important this decision is and how a poor credit score can make it hard to achieve. That's why we offer personal loans ranging from $100 to $1,400, even if you have low, bad, or no credit history.

Apply online for a personal loan with us today! Our online application process is swift and easy, and we'll keep you fully informed of every detail along the way. If you're in Oklahoma, Texas, or Virginia and prefer to do things in person, visit one of our physical locations to start your application process.